Quick answer

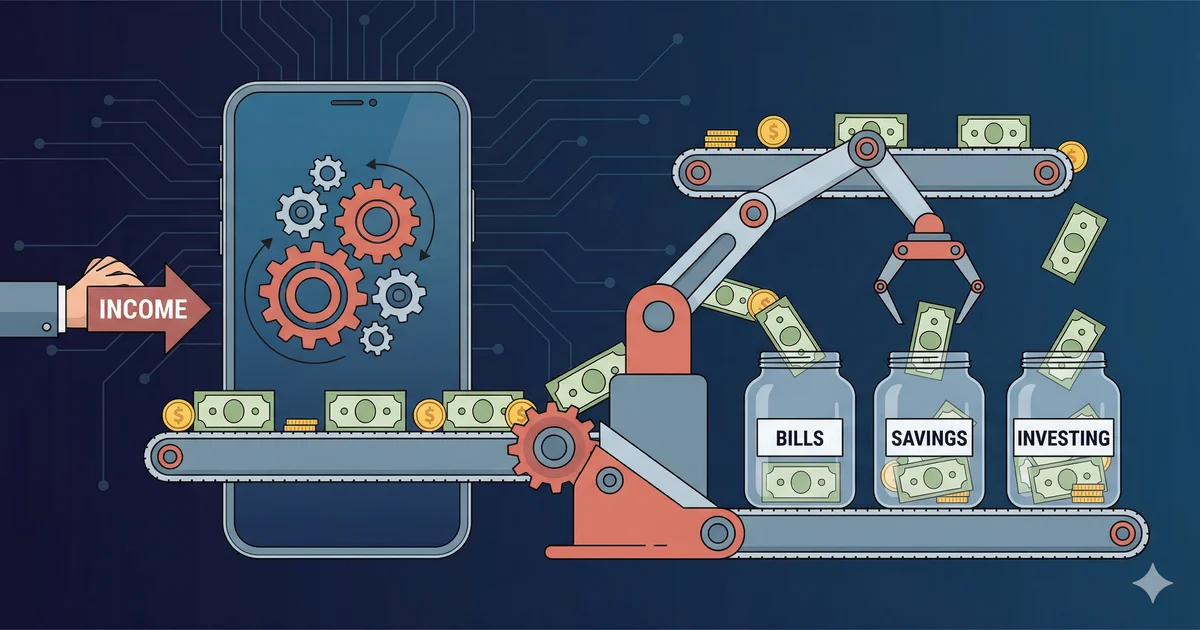

The secret to building wealth is not willpower — it is automation. When saving, investing, and bill-paying happen automatically, you remove the largest barrier to financial success: human psychology.

The secret to building wealth is not willpower — it is automation. When saving, investing, and bill-paying happen automatically, you remove the largest barrier to financial success: human psychology.

Why Automate Your Finances?

- No missed payments: Autopay eliminates late fees (Americans pay $12 billion in credit card late fees each year)

- Consistent saving: Automated savers accumulate 30–40% more than manual savers

- Reduced stress: Once set up, money flows to the right places without daily decisions

- Better credit score: On-time payments (35% of your score) become effortless

- Time saved: One 60-minute setup session replaces hours of monthly bill management

The Automation System

- Paycheck deposits to checking account

- Auto-transfer to savings (20%)

- Auto-transfer to investment account

- Auto-pay bills and debt payments

- Remaining = guilt-free spending money

Step-by-Step Setup Guide

Step 1: Map Your Money Flow

List every source of income and every recurring expense. Note the date, amount, and whether it is fixed or variable.

Step 2: Set Up Automatic Savings

| Savings Goal | Where | When | Amount |

|---|---|---|---|

| Emergency fund | High-yield savings | Payday | $200/paycheck |

| Retirement (401k) | Employer plan | Each paycheck | 10–15% pre-tax |

| IRA | Brokerage | 1st of month | $500/month |

| Sinking funds | Separate savings | Payday | $100–$300 |

Step 3: Automate Bills

Set up autopay for every recurring bill:

- Rent/mortgage (fixed — schedule for the 1st)

- Utilities (autopay from provider — variable amounts)

- Insurance premiums (fixed monthly or annual)

- Subscriptions (already auto-charging — just verify)

- Loan/debt payments (set to pay more than minimum automatically)

Step 4: Automate Investments

Set up automatic contributions to your brokerage or IRA. Most platforms let you set up regular purchases of index funds or ETFs on a schedule. This is dollar-cost averaging — the simplest, most effective investing strategy.

Step 5: Create a Buffer

Keep $500–$1,000 extra in your checking account as a buffer. This prevents overdrafts if timing does not line up perfectly between payday and automated withdrawals.

Sample Automation Calendar

| Date | Action | Amount |

|---|---|---|

| 1st | Rent/mortgage autopay | $1,500 |

| 1st | Auto-transfer to IRA | $500 |

| 5th | Auto-transfer to emergency fund | $200 |

| 5th | Auto-transfer to sinking funds | $150 |

| 10th | Insurance premium autopay | $200 |

| 15th | Utility autopay | ~$150 |

| 15th | Second paycheck deposits | $2,500 |

| 16th | Auto-transfer to savings | $200 |

| 20th | Student loan autopay | $300 |

| 25th | Credit card autopay (full balance) | Varies |

Worked Example: Sarah's First Month on Autopilot

Sarah earns $4,800/month after tax, lives in Austin, and pays $1,500 rent plus $700 in fixed bills. Before automation, she ran her checking down to $40 every cycle and saved nothing. Here is what changed in her first 30 days after setting up the system.

| Day | What ran | Where it went |

|---|---|---|

| 1 | Paycheck #1 deposits ($2,400) | Checking |

| 1 | Rent autopay | $1,500 out |

| 3 | Auto-transfer to high-yield savings | $240 (10%) |

| 3 | Auto-transfer to Roth IRA | $300 |

| 5 | Utilities, internet, insurance autopay | $320 out |

| 10 | Credit card autopay (full balance) | $420 out |

| 15 | Paycheck #2 deposits ($2,400) | Checking |

| 16 | Auto-transfer to savings + IRA | $540 |

| 20 | Sinking fund transfer (car, gifts) | $120 |

| 30 | Buffer remaining in checking | ~$760 spending money |

The result: Sarah saved $1,080 in month one without thinking about it. The same income, the same bills, just a different order of operations. Repeated for 12 months, that pattern adds about $13,000 to her net worth before any raises or compound growth.

Five Automation Mistakes That Cost People Money

- Setting transfers for the same day as payday. Direct deposits sometimes post late, especially over weekends or federal holidays. Schedule transfers 1 to 2 business days after expected paydays so the money has actually arrived before it tries to leave.

- Automating only minimum payments on debt. Autopay is set-and-forget, which is exactly the problem if you only auto-pay minimums. Auto-pay the full statement balance on credit cards, or a fixed dollar amount above the minimum on installment loans.

- Skipping a six-month subscription audit. Subscriptions silently raise prices. Old gym memberships keep charging. Twice a year, pull the last 90 days of statements and cancel anything you used fewer than four times.

- Running a $0 buffer. An empty checking cushion guarantees an overdraft the first time a bill posts a day early. Keep $500 to $1,000 idle as a permanent buffer; it is not savings, it is plumbing.

- Auto-investing without checking allocations. Target-date funds drift, contribution limits change, employer matches occasionally get capped. Once a year, log into the brokerage and confirm contributions, allocations, and beneficiary designations.

Frequently Asked Questions

What bills should I automate first?

Fixed-amount bills: rent, insurance, loan payments, and subscriptions. Then automate variable bills like utilities.

Is automating savings really effective?

Yes. Automated savers accumulate 30–40% more than manual savers because money moves before you can spend it.

What if I overdraft from too many automatic payments?

Keep a $500–$1,000 buffer in checking. Schedule transfers 1–2 days after payday and review monthly.

Should I automate investments?

Absolutely. Dollar-cost averaging through automatic monthly contributions removes emotion from investing.

How often should I review my automated system?

Monthly for the first 3 months, then quarterly once everything runs smoothly.