Quick answer

Most people budget by guessing. They estimate what they will spend and hope it works out. Then they wonder where their money went. Zero-based budgeting is the opposite: you plan where every single dollar goes before you spend it.

Most people budget by guessing. They estimate what they will spend and hope it works out. Then they wonder where their money went. Zero-based budgeting is the opposite: you plan where every single dollar goes before you spend it.

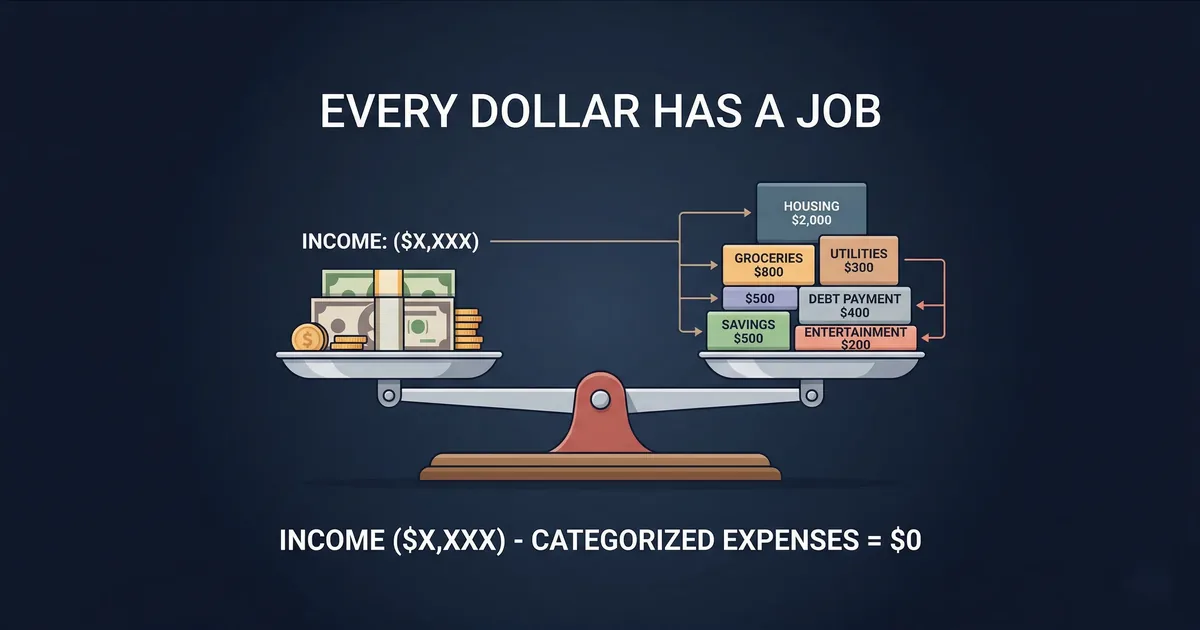

The principle is simple: income minus expenses equals zero. That does not mean you spend everything and have nothing left. It means every dollar has a specific assignment — whether that is rent, groceries, savings, or fun money. Nothing is left floating without a purpose.

What Is Zero-Based Budgeting?

Zero-based budgeting (ZBB) is a method where you assign all of your income to specific categories. You keep going until your remaining balance is zero. With traditional budgeting, you might only track a few categories and ignore the rest. ZBB requires you to plan for every dollar on purpose.

Monthly Income − (Needs + Wants + Savings + Debt Payments) = $0

Every dollar gets a job. No dollar is left unassigned.

This idea started in business accounting in the 1970s. Peter Pyhrr at Texas Instruments created it to review and justify every expense each year. Personal finance teachers later brought it to household budgeting. The Consumer Financial Protection Bureau now recommends zero-based approaches for people who want full control of their money.

How Zero-Based Budgeting Works

Before each month starts (or before each paycheck), you plan how to spend every dollar you expect to earn. Here is the key difference from other methods:

- Traditional budgeting: Set limits on a few categories, hope for the best, check at month end

- 50/30/20 budgeting: Split income into three broad buckets — see our 50/30/20 budget rule guide

- Zero-based budgeting: Assign every dollar to a specific, detailed category with nothing left over

The zero-based approach takes the most effort. But it works best for people who overspend or feel like money disappears for no clear reason.

Step-by-Step: Create Your First Zero-Based Budget

-

Step 1: List All Income Sources

Write down every source of income for the upcoming month: salary, side hustles, freelance payments, child support, investment income. Use your after-tax amount — the money that actually arrives in your bank account.

If your income varies, use the lowest amount you reasonably expect. You can allocate bonus income when it arrives.

-

Step 2: List Every Expense Category

Write down everything you need to spend money on. Be specific — instead of "food," break it into "groceries" and "dining out." Common categories include:

- Rent/Mortgage

- Utilities (electric, gas, water, internet)

- Groceries

- Transportation (gas, transit, car payment)

- Insurance (health, auto, renters)

- Minimum debt payments

- Dining out

- Entertainment/subscriptions

- Clothing

- Personal care

- Emergency fund contribution

- Retirement savings

- Extra debt payments

- Gifts/donations

- Miscellaneous/buffer

-

Step 3: Assign Dollar Amounts

Go through each category and assign a specific dollar amount based on your actual needs for that month. Start with fixed expenses you must pay (rent, insurance, minimum payments). Then cover changing costs (groceries, utilities), then wants, then savings goals.

-

Step 4: Make It Equal Zero

Add up all your planned expenses and compare to your income. If income minus expenses is positive, allocate the remaining dollars to savings or debt repayment. If it is negative, cut from want categories until you reach zero.

Important: Zero does not mean you are broke. It means every dollar is working — including the dollars going into savings.

-

Step 5: Track Throughout the Month

The budget is only useful if you track your expenses against it daily. Log every transaction and categorize it. When a category runs out, stop spending in it or move money from another category.

Zero-Based Budget Example ($4,500/Month)

| Category | Budgeted |

|---|---|

| Rent | $1,300 |

| Utilities | $150 |

| Groceries | $400 |

| Transportation | $250 |

| Insurance | $200 |

| Minimum Debt Payments | $150 |

| Dining Out | $200 |

| Entertainment | $100 |

| Clothing | $75 |

| Personal Care | $50 |

| Subscriptions | $45 |

| Emergency Fund | $300 |

| Retirement (IRA) | $500 |

| Extra Debt Payment | $200 |

| Gifts | $50 |

| Miscellaneous Buffer | $30 |

| Total | $4,500 |

| Income − Expenses | $0 |

Pros and Cons of Zero-Based Budgeting

Advantages

- Total awareness: You know exactly where every dollar goes

- Eliminates waste: No money slips through the cracks

- Highly customizable: Adjusts to any income level or financial goal

- Forces prioritization: You must decide what matters most each month

- Accelerates debt payoff: Every spare dollar can be directed at debt using strategies like the debt snowball or avalanche method

Disadvantages

- Time-intensive: Requires more planning than simpler methods

- Difficult with irregular income: Harder when you do not know exact income ahead of time — see our guide to budgeting on irregular income

- Can feel restrictive: Some people find the detailed tracking stressful

- Monthly reset required: You must create a new budget every month

Tips for Zero-Based Budgeting Success

- Budget before the month begins: Sit down in the last few days of the previous month to plan ahead. Building this into your routine helps you develop lasting financial habits.

- Include a miscellaneous buffer: A $25–$50 "miscellaneous" category handles small surprises without derailing your budget.

- Use a budget tracker app: Budget Lock lets you create detailed categories and track spending against each one with visual progress rings.

- Adjust mid-month when needed: Life happens. Move money between categories rather than abandoning the budget entirely.

- Give it three months: The first month is the hardest. By month three, you will have a much better feel for your spending patterns.

When Zero-Based Budgeting Falls Short

Zero-based budgeting is the most rigorous of the major systems, which is also why it fails for some users. The method demands that every dollar gets a category before the month begins. That structure is a feature for some people and a friction trap for others.

- Variable income. ZBB assumes a known income figure at the start of each month. Freelancers, commission workers, and gig drivers should run the buffer-account method from our irregular income guide instead, then optionally apply ZBB to the buffer-paid "salary" only.

- You hate categorization. If reviewing 60+ transactions a month and assigning each to the right envelope sounds like punishment, you will skip it after six weeks. The pay-yourself-first method requires almost no maintenance and captures most of the same savings benefit.

- Couples with mismatched spending styles. ZBB only works if both partners agree on category limits in advance. If one wants every coffee categorized and the other wants a single "fun money" line, agree on a hybrid: joint categories for fixed bills, individual allowances for everything discretionary.

- You are mid-emergency. Job loss, medical event, or a surprise expense changes priorities daily. Switch to a 2-tier survival budget (essentials only + buffer for the unknown) until the crisis ends, then return to ZBB.

Frequently Asked Questions

What is zero-based budgeting?

Zero-based budgeting is a method where your income minus all planned expenses equals zero. Every dollar is assigned a specific job — bills, groceries, savings, or fun money. Nothing is left unallocated.

Is zero-based budgeting good for beginners?

Yes. While it requires more upfront effort than simpler methods, it gives you complete control and builds strong financial awareness from day one.

How is zero-based budgeting different from traditional budgeting?

Traditional budgets carry over last month's numbers. Zero-based budgeting starts fresh each month, requiring you to justify and plan every dollar based on that month's specific needs.

What if I have money left over in my zero-based budget?

Assign it to a category — extra savings, debt payoff, or next month's buffer. The goal is for income minus expenses to equal exactly zero.

Can I do zero-based budgeting with irregular income?

Yes. Budget based on your lowest expected monthly income. When you earn more, allocate the extra to priority goals. List expenses by importance so you know what to fund first.